| Welcome to the September issue of the Select Wealth Management Dashboard Newsletter. This week marks a significant turning point in the financial markets. The Federal Reserve (America's Reserve Bank), cut interest rates for the first time since March of 2020 (4 ½ years). This is welcome relief for households and business.

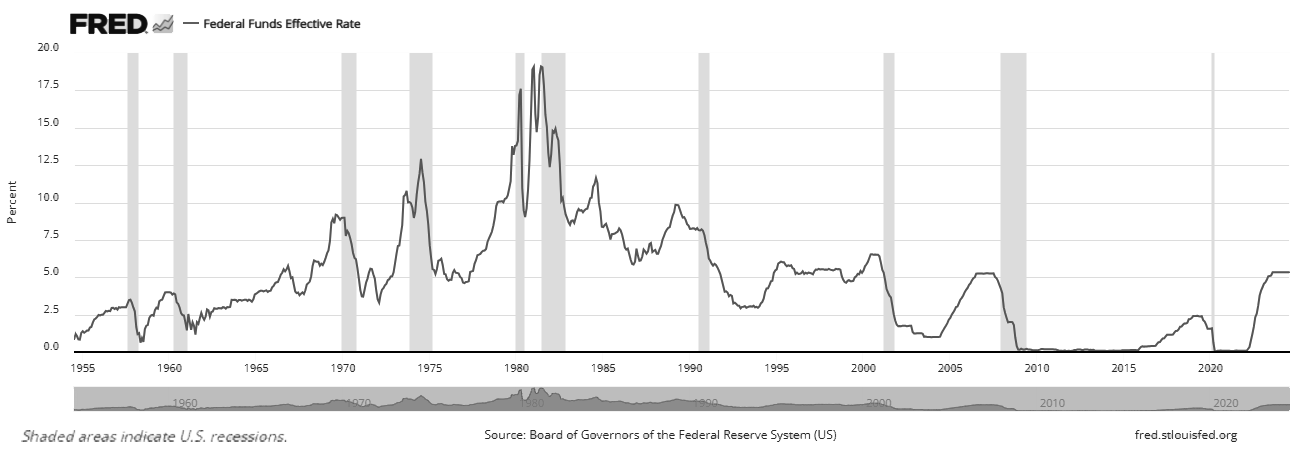

Let's do a quick recap on how we got here... Covid took hold in early 2020 forcing many countries into lockdown. At the time, Central Banks around the world were (rightly) extremely concerned that economies were going to collapse, so their response was to slash interest rates (to 0% in many countries). In many cases, governments also gave financial assistance to people (think back to the "Wage Subsidy" paid to businesses and "Cost of Living Payments" made to individuals in NZ). This flooded the financial system with money. Time went by and economies came out of lockdowns. After being locked up for months, we all rushed out and bought new cars, campervans, holidays, bigger houses, So now Reserve Banks around the world were forced to raise interest rates from these historical lows in an effort to combat inflation. And they raised them aggressively - super aggressively. In fact, in New Zealand the Reserve Bank raised the Official Cash Rate (OCR) from 0.25% in October 2021 to 5.50% in May 2023. Not only was this the largest increase in the OCR since records began 25 years ago, but it was also at the quickest pace (a 5.25% increase in 595 days). Many other jurisdictions followed a similar pattern. This caused significant pain in the real economy. Suddenly everyone's mortgage rolled over from 2% to 7%, and every dollar of discretionary spend had to be re-directed to making mortgage payments. No more dinners out, coffees, new toys, holidays, On reflection, the past 5 years were a real roller coaster ride. We went from hyper cheap money and easy living in 2021 (house prices sky-rocketing, inflated investment returns, and real purchasing power) to a cost of living crisis and tough economic times in 2022 / 23. But my sense is that we are entering a period of normalisation now. Inflation is under control, central banks are starting to cut rates, and moderation is emerging. This is extremely healthy in my opinion. I am now watching with interest to see how far rates come down. We want a Goldilocks cycle - not too hot, not too cold, but juuuust right. The below chart shows historic interest rates in the USA since 1955:  Click here to view full size image

Click here to view full size image

You will notice (at the right of the chart), that the current rate is higher than the average over the past 30 or so years, but actually not too far off the average for the whole period (since 1955). So my sense is that there is more relief to come, but we are definitely not going back to the unusually low rates of the past decade. The Federal Reserve's own forecasts imply a neutral rate of about 3% (a further reduction of 2% from today) by the end of 2026. If that's where we end up, I would be very happy with the outcome. That would mean mortgage rates of about 4% - 5% (juuust right), borrowing costs for businesses being reasonable enough for good businesses to prosper but poor business to fail (juuust right), and investment markets to return to fundamentals rather than reply on stimulus (juuust right). The next 6 to 12 months of this journey will be pivotal. In terms of the markets, the past 30 days have been mixed. The Australian, German and American share markets were all up strongly, but the London, New Zealand and Japanese stock markets were all down. The New Zealand dollar strengthened against most of its trading partners, and house prices fell a bit further. Mortgage and term deposit rates continue to slide downwards, and this trend is expected to continue for the foreseeable future. Here are the numbers for the past 30 days: |

||||||

|

||||||

In terms of your Select Wealth Management portfolio, you will receive your performance report for the 30 September quarter early next month. Performance has been strong for the quarter so far, and failing any major sell-off in the remaining 6 trading days, it will be another strong quarter (and year). A major development for some clients this quarter has been the successful capital raise for Synlait Milk Ltd. Late last year, Makowem & Isaacs Financial Planning made a recommendation to many clients to buy the Synlait Milk Bond (SML010) which was trading at a significant discount. It was confirmed earlier this week that the bond will be repaid on 14 November at full face value (the outcome we always believed was most likely). This resulted in a very healthy return of about 18% over the past year on this investment for those who participated. We continue to look for these opportunities and will always let you know if we find one that we believe is appropriate for your portfolio. Finally, a quick update on our Giving Back program. We are now nearly half way through the campaign for Life Flight, and we have raised $780 so far. We have until the end of the year to try reach our target of $2,500. As always, thank you so much for the introduction to your friends and family to allow us to continue this program. We really appreciate it! Feel free to visit https://mifinancialplanning.co.nz/giving-back.html if you want to keep track of the Giving Back program. That's all for now. Chat again soon Warm regards Dave and the team at Makowem & Isaacs Financial Planning dave@mifinancialplanning.co.nz |

||||||

|

||||||

This newsletter is intended for general distribution and does not constitute personal financial advice.