| Welcome to the Select Wealth Management October issue of the Dashboard Newsletter. The past month has been action packed. The All Blacks beat Ireland to make the semi finals of the Rugby World Cup and the Black Caps march on towards the semi finals of the Cricket World Cup. Unfortunately the Silver Ferns and All Whites fared less well against Australia in the Netball Constellation Cup and Football International, both soundly beaten. But the most significant result was of course the change in Government from centre left to the centre right.

This time round, there was a vote for change. As such, a yet to be confirmed centre right coalition will soon take the reins with the aim of "moving the country in a different direction" (quote). As is often the case after an election, the reality is that just over half the population are delighted with the outcome, and just under half are disappointed. My read on the mood of the nation in the past 12 months has been that there was a sense of division and a lack of national unity. Irrespective of your political leanings, my hope for the new government is that they are able create a more unified national identity - one where poor behaviour (negative contribution to society) faces consequence, and success is celebrated. The obvious question I am being asked a lot at the moment is "how will the change of government affect my investment". The short answer is "not a lot". There are a range of reasons for this. Firstly, if you think about it, a typical Balanced Portfolio only has about 33% exposure to the New Zealand economy - normally about 10% in New Zealand Shares, 20% in New Zealand fixed interest and a bit in New Zealand property. The other 67% is in offshore investments that are unaffected by New Zealand politics. So even if a change in government did have an impact, it would only affect about 1 third of your total investment. Secondly, despite popular perception, most business sectors are reasonably unaffected by changes in government. There are exceptions to the rule, but this will typically stem from clearly publicized reform to a particular sector. For example, the incoming government has signalled that they will repeal some of the changes that were made in the past 5 years targeting property investors. They plan to reduce the Brightline test back to 2 years, allow foreign buyers back into the market, and allow interest deductibility again. This has an immediate and direct impact on property investment - so expect the property market to be more buoyant in the short term moving forward. On the flip side of that, government spending is clearly going to reduce in the next 3 years, so some sectors exposed to this will feel some pain. But aside from these targeted changes, most industry and commerce will continue as before. There will be some slight winners, and some slight losers, but on balance, the wheels of commerce continue to turn. Widget makers continue to make widgets, cafes continue to sell coffee, and IT Consultants continue to consult. To illustrate the point, the below table plots the returns of the NZX50 (the New Zealand share market) since inception in 2002 against the government of the day.

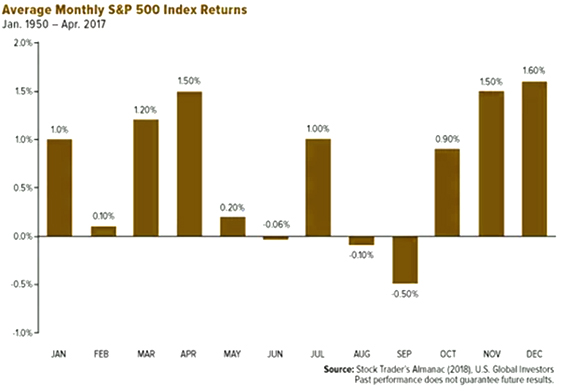

You will note that there is no correlation between returns and government. A Labour coalition has both the best returns (+74% from 2002 to 2005) and the worst return (-18% from 2005 to 2008 - leading into the global financial crisis). The point is that share market returns are far more driven by general business conditions (interest rates, global growth rates, availability of capital) and global events (oil price shocks, conflict / terror attacks, weather events, global financial crises) than they are by changes in government. Encouragingly, it's worth noting that overall, returns are typically positive over any 3 year term, and that the magnitude of the positive returns is far greater than that of the negative - a very compelling case for investing in shares. So as is typically the case in these situations, my advice is to ignore the background noise and focus on the things that you can control. Is your investment consistent with your appetite and capacity for risk? Are you saving enough / too much to meet your retirement goals, or spending too much / not enough if you are in retirement? Are you monitoring your progress against your financial plan. If you get these basics right, you will have an enjoyable retirement irrespective of who is in government. In terms of the markets, September was a very challenging month. September is typically the worst month of the year for share markets (as evidenced by the below chart), and this year was no different.

The S&P500 (American share market) fell by 4.28% in the month of September - a blemish for the quarters returns eroding all the gains from July and August. Historically, the December quarter is usually the best (known as the Santa rally), so if the trends hold true this year, we'll have a decent rally into year's end. Here's hoping! Here are the numbers for the past 30 days: |

|||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||

You will by now have received your September quarterly reports for your Select Wealth Management portfolio. It was a frustrating quarter which started well, but gave all the gains made in July and August back in September. Despite the poor quarter, the annual returns are still respectable. Most importantly, I remain absolutely confident in the positions of our portfolios - particularly those with a higher exposure to fixed interest. With interest rates around the western world looking close to the top of the cycle, we are well positioned to enjoy meaningful returns in the medium term. Patience will be rewarded. Finally, a quick update on our Giving Back program. Our campaign for the Billy Graham Youth Foundation is going really well, and we are now up to just over $1,650 for this great cause. I am confident that we will achieve our goal of $2,500 by the end of the year. As always, thank you for the introduction to your family and friends which enables us to keep this program running. To keep track of the Giving Back program visit https://mifinancialplanning.co.nz/giving-back.html Warm regards Dave and the team at Makowem & Isaacs Financial Planning dave@mifinancialplanning.co.nz |

|||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||

This newsletter is intended for general distribution and does not constitute personal financial advice.