| Welcome to the October issue of the Dashboard Newsletter.

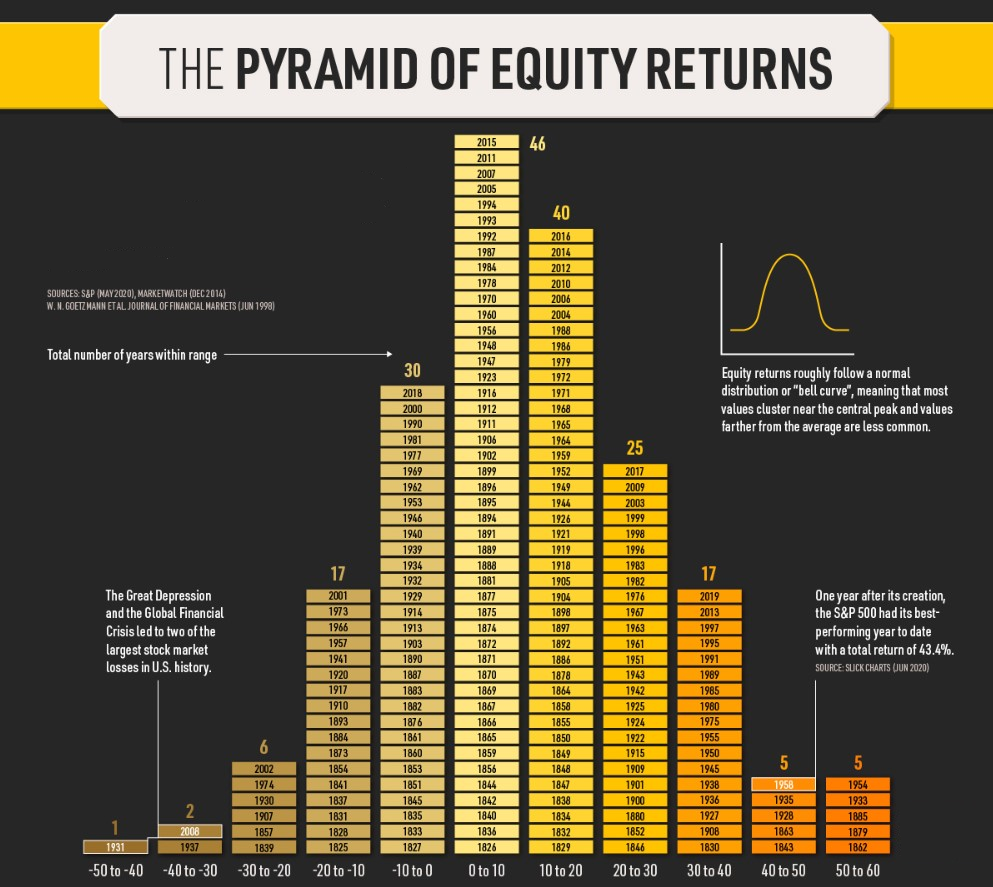

Well, we're on the home straight to year's end now. The 3rd quarter of the year has come and gone, and the next stop involves Christmas stockings and sleigh-bells. Every year at about this time, I promise myself I'll be organised and get my Christmas shopping done nice and early. Yet every year I find myself scrambling around shopping centres the week before Christmas doing last minute shopping. Surely this year will be different... One thing that has been different so far this year is investment returns. I've been investing money on behalf of clients for over 20 years now. I cut my teeth through the Global Financial Crisis of 2008, and as a result of this have always been a very cautious investor - I know how painful investing can be. I can safely say that 2022 so far has been as challenging a year as I can recall. There really has been no place to hide. To illustrate the point, consider the following table which outlines the return of the American stock market in any given calendar year over the past 194 years (from 1825 to 2019).

This table illustrates that the most common return from the American stock market in any given calendar year is between 0% and 10%. This occurred 46 times. The next most common was returns between 10% and 20%, which occurred 40 times. In contrast to this, there were 30 occasions where the returns were between 0% and -10%, and 17 occasions where the returns were between -10% and -20% in any given year. There are a few interesting points to note from this table. Firstly, there are far more occurrences of positive returns (138) than negative returns (56). This is relatively obvious - share markets go up more than they go down. Otherwise why invest? Secondly, the magnitude by which they go up (when they go up) is greater than the magnitude by which they go down (when they go down). As an example, markets have never fallen in value by more than 50% in any given calendar year, yet they have grown in value by more than 50% on 5 occasions. So they go up more often than they go down. And when they go up, they go up a lot - more than they fall in value from time to time. That sounds like a compelling investment to me. These 2 observations are obvious, and relatively common knowledge. Tune into any financial media, and you would hear similar stats and anecdotes all the time. But the thing that caught me a bit by surprise was this: Year to date so far, the S&P500 (the American share market), is down 24.95%. That puts 2022 firmly in the -20% to -30% category - something that has only happened 6 times in the past 194 years. That validates my sense of this year having been one of the most challenging in a very, very long time. Granted, we have 2 ½ months to go before the end of the year, and at the rate markets are moving we could easily move out of this bracket and into another (either for better or worse). But as it stands, we would add the 7th bar to the -20% to -30% return bracket. And what makes 2022 even more challenging is the fact that it's not just the share markets that have fallen in value. Interest rates (the OCR) started the year at 1%, and have now shot up to 3.5%. The effect of this is that bonds (fixed interest) have also delivered negative returns so far this year. Even the values of our homes have fallen by about 15% this year. So every component of a typical Balanced Portfolio has fallen in value. It's no wonder it's felt so tough... So what should we make of all of this. Well, nothing really - they are just interesting observations. It's been a very challenging year so far. Could it get worst? Sure it could. History suggests that it is unlikely to get too much worse, but it could... History also suggests that if you have the capacity to ride it out, you will end up on the right side of it. Markets go up more than they go down, and in greater magnitude. But that doesn't take away the fact that this year, you could be forgiven for feeling like your investment has been very, very painful... It has. In terms of the markets, the past month has seen continued weakness. Share markets are down between 3% (Australia) and 11% (Hong Kong). Currencies remain extremely volatile too, with the NZ$ weakening against most major trading partners. The NZ$ briefly dipped below US$0.55 this month - the lowest it has been in nearly 15 years. Shopping on Amazon is a lot more expensive these days.... Here are the numbers for the past 30 days: |

||||||

|

||||||

In terms of your Select Wealth Management portfolio, you will soon be receiving your September quarter performance reports. After a very strong July and a flat August, I was hoping to deliver a positive return for the September quarter. However, the month of September was particularly brutal for investment markets, and wiped out all of July and Augusts gains meaning that unfortunately most portfolios will have negative returns again for the quarter. We remain comfortable with our portfolio positions, and continue to deploy cash into the fixed interest market. When the opportunity presents, we will also re-balance back into share markets. Finally, a quick update on our Giving Back program with Kaibosh. Progress remains slow given the challenging environment, but we are still working hard in an effort to make a meaningful contribution to this great cause. It's unlikely we will reach our target of $2,500, but hopefully we will get something close to it. To keep track of the Giving Back program visit https://mifinancialplanning.co.nz/giving-back.html As always, thank you for your continued support by introducing friends, family and colleagues to our business as prospective clients - I really appreciate it. Warm regards Dave and the team at Makowem & Isaacs Financial Planning dave@mifinancialplanning.co.nz |

||||||

|

||||||

This newsletter is intended for general distribution and does not constitute personal financial advice.