| Welcome to the May issue of the Dashboard Newsletter. The past month has seen continued volatility in all investment markets. Share, bond and property markets experienced another month of heavy losses, and speculative assets such as crypto currencies have capitulated. It is a painful and unsettling time for any investor.

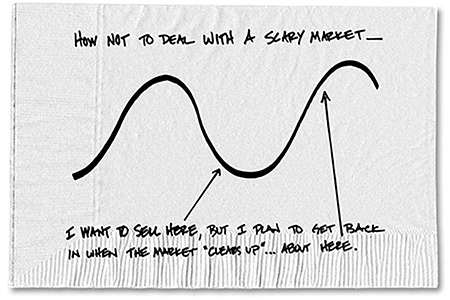

At times like these, people often turn to investment professionals hoping for a "quick fix" to the problem - a magic silver bullet to make the pain go away. But the reality is that there is no such thing - and beware the messenger who tells you otherwise, lest you end up with snake oil. So perhaps my message in this month's newsletter is not what you want to hear, and perhaps you'll feel like it's not at all dynamic, but in my 20 years experience and my study of the past 100 years of market data, this boring message always wins out over time... Here are my simple principles to getting through this tough market: 1. Stay disciplined, and stick to your plan When markets are volatile and headlines are all negative, it's easy to measure performance in 1 month increments. But remember, your investment is solving a multi decade problem, not a 1 month problem. The real question should be "Will my investment still create the retirement lifestyle I want over the next 30 years?", not "what was the performance last month?". 2. Don't panic This old cliché is best illustrated by Carl Richards in this diagram:

3. Use the magic of "Dollar Cost Averaging" Dollar Cost Averaging refers to the concept of buying investments over different periods of time at different prices. Volatile markets can actually enhance your returns when you do this. To illustrate the point, consider an investment where you contribute $1,000 per month over a period of 12 months. In scenario A, the unit price starts at $1, and gradually increases over the 12 month period to $1.05. In scenario B, the unit price starts at $1, and falls in value before recovering to $1 again.

So even though scenario A ends at a higher unit price ($1.05), the total value after 12 months is lower than scenario B with a unit price of $1.00. This is great if you're making regular contributions, but what if you're making regular withdrawals? This principle works in reverse too. You've been selling units at higher unit prices in the past, so you've locked in those gains forever. Over long periods of time, you get the benefit both ways. 4. Be brutally honest when risk profiling I can't emphasize the importance of this enough. Filling in a quick multichoice questionnaire online isn't thorough enough. You need to really understand the risks involved with your investment before you commit. What can you reasonably expect from this investment - in both good times and bad. Do your genuinely have the stomach to tolerate the volatility when it happens (because volatility is inevitable). This is why I always labour the point of our risk profiling conversations and force you to update it regularly. This may seem tedious at times, but if we get it right, your investment should never deliver an outcome that surprises you. There will be times of discomfort for sure (like now), but these shouldn’t be outside of what your risk profile indicated you could stomach. So there you have it - some simple, boring tips to help you navigate this challenging time. If you want to discuss any of these, or just want to meet to go through your portfolio, give us a call - we are here to help. Here are the numbers for the past 30 days: |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In terms of your Select Wealth Management portfolio, there is not a great deal to report at this stage. Our researchers JMI Wealth continue to do a lot of work behind the scenes, and we are implementing small incremental changes from time to time to navigate the current environment. The general theme is to keep portfolios more or less neutral, and to bias New Zealand fixed interest relative to global fixed interest (given that our rates are slightly higher than global rates at this stage). By now you should also have received your tax reports for those of you who need these. Finally, a quick update on our HUHA (Helping You Help Animals) Giving Back program. We are coming towards the end of this campaign (running to June 2022), and putting in a late charge to reach our target of $2,500. To keep track of the Giving Back program visit https://mifinancialplanning.co.nz/giving-back.html As always, thank you for your continued support by introducing friends, family and colleagues to our business as prospective clients - I really appreciate it. Warm regards Dave and the team at Makowem & Isaacs Financial Planning dave@mifinancialplanning.co.nz |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

This newsletter is intended for general distribution and does not constitute personal financial advice.