| Welcome to the June issue of the Select Wealth Management Dashboard Newsletter. One of the most common questions I get asked as a Financial Planner, both in a professional capacity in my office and a personal capacity around the BBQ, is "How much do I need to retire?". It's a very common and rational concern - will I have enough?

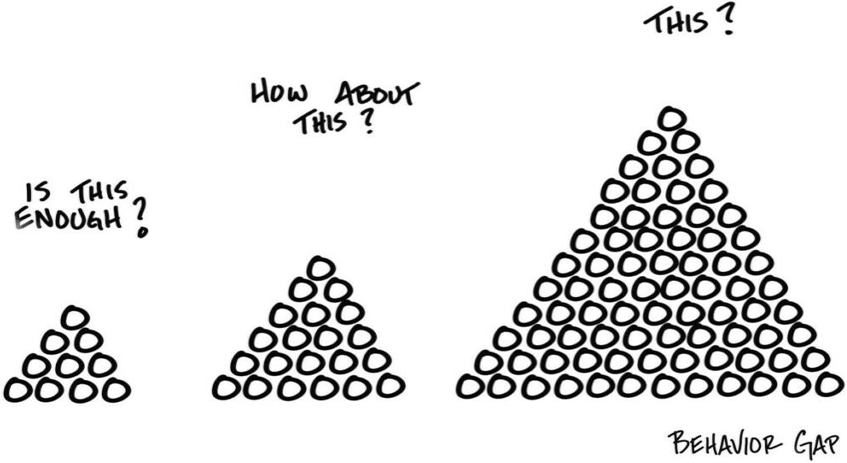

There is a great anecdote about this. Kurt Vonnegut and Joseph Heller were at a party hosted by a billionaire hedged fund manager on Shelter Island. Kurt turns to Joseph and says "You know, our host reportedly made more money in 1 day of trading than you made from all the sales of your wildly popular novel Catch 22". Joseph calmly responds "Yes, but I have something he will never have... enough.". I love this story. It draws the focus away from a simple measure of quantity (more and more), to thinking about context (do I need more and more, or do I have enough). Carl Richards draws it like this:

Enough is an interesting amount. For a start, it's different for everyone. I have clients who can live comfortably on $30,000 per year, and others who can't on $300,000 per year. Their "enoughs" are clearly poles apart. Interestingly, the people who live on $30,000 a year often have a pile of money that looks like the pile on the right of Carl's picture. They are so worried that they don't have enough that they forego experience and comfort in an effort to accumulate more. And similarly, the people spending $300,000 per year often have a relatively small pile of money and will run out at a relatively early age. Neither of these approaches are winning at life... The best value that a good Financial Planner can offer you is helping you understand your enough. How much capital do you need, and what return is required on this capital, to achieve all the things you want to achieve in life. Most people have an arbitrary value in their minds - something like $1 million or 10 times my annual salary. The only goal they have is to get the best return possible to reach their arbitrary target as quickly as possible. But the conversation should be less about stocks and bonds, returns, or fund x versus fund y, and more about your goals and aspirations. Questions like:

In terms of the markets, the past 30 days have been challenging for shares. Markets range from flat (New Zealand) to down 5 ½% (Hong Kong). Exchange rates are relatively muted, and mortgage and deposit rates have remained unchanged. Here are the numbers for the past 30 days: |

||||||

|

||||||

In terms of your Select Wealth Management portfolio, we have existed all positions from the Castle Point Ranger Fund (you will have been contacted if you were affected by this). This comes after running out of patience after a year of close scrutiny and negative watch. We remain comfortable with all other fund managers, and there are also some new fund managers being included on our panel of approved managers, including Daintree and Schroder. Finally, a quick update on our Giving Back program for Ellie's Rescue and Rehome. We are nearing the end of the campaign (30 June), and unfortunately it looks unlikely that we will reach our target of $2,500. However, I am pleased to confirm that we will be able to make a donation of at least $2,000 to this wonderful cause. Thank you Ellie's for the great work you guys do. If you are someone you know is looking for a new 4 legged best friend, be sure to check out https://www.elliesk9rescue.co.nz/adopt.html As always, thank you so much for the introduction to your family and friends to allow us to continue this initiative - we really appreciate it. We will have a new campaign to share with you next month. In the meantime, to keep track of the Giving Back program visit https://mifinancialplanning.co.nz/giving-back.html That's all for now. Chat again soon Warm regards Dave and the team at Makowem & Isaacs Financial Planning dave@mifinancialplanning.co.nz |

||||||

|

||||||

This newsletter is intended for general distribution and does not constitute personal financial advice.