| Welcome to the June issue of the Dashboard Newsletter. As we approach the halfway mark of the year and stare winter in the face, it's fair to say that it's been a tough 24 hours for Kiwi sports fans. The Black Caps are up against a resurgent English cricket team, and the All Whites' world cup dream slipped away in a 1-0 defeat to Costa Rica. Whilst the results didn't go our way, both games were a fantastic spectacle, and both teams (the All White's particularly) gave it a real crack boxing way above their weight. The future of New Zealand football is bright.

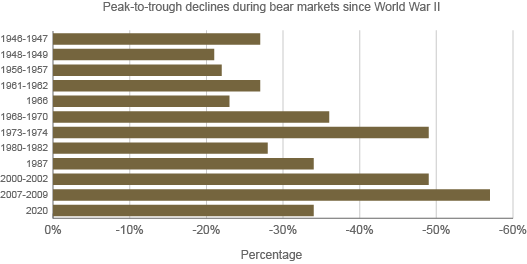

The markets have been as stormy as our winter weather over the past month. Last night, the S&P500 (a measure of the American stock market) entered "bear market" territory. The definition of a bear market is "a fall of 20% or more from the most recent highs". The S&P500 reached a high of 4,766 on 27 December 2021, and closed last night at 3,749 - a fall of 21.3%. This might sound alarming, but the reality is that it happens quite frequently. Since WW2, the S&P500 has been through 12 bear markets - so a bear market every 6 ½ years. The biggest decline was 57% during the Global Financial Crisis of 2007 & 2008, and the smallest were falls of 20.6%; 21.5% and 22% in 1948; 1956 and 1966 respectively. The average decline across all 12 bear markets was 33%.

So how long does it take for the market to recover? Well, the quickest recovery from a bear market was 23 trading days. This was the ultra sharp correction after the "false bear" in 2020 from the COVID pandemic scare. The longest was 637 trading days after the DotCom boom and bust of the 2000's. The average time across all 12 bear markets was 285 trading days (or just over a year).

What's made this bear market even more challenging is the fact that it has predominately been driven by very sharp interest rates rises. The relevance of this is that sharply rising interest rates have a (short term) adverse effect on fixed interest (bonds). So even fixed interest has delivered a negative return for the calendar year. (The New Zealand Bond index is down over 5% for the year to date at the end of May). So, if you have a Balanced Portfolio with half the money in shares and the other half in bonds, you would normally expect the bonds to offer some reprieve when share markets sell off. But this time, both the share market and bond portion of the portfolio has delivered negative returns. Whilst bear markets happen relatively frequently, it doesn't make them any easier to handle. It's horrible watching your investment fall in value. And it's extremely difficult to stand by and do nothing with the aim of riding it out - even for the most seasoned investor. Doing nothing seems extremely counter-intuitive. But there is an old saying, "In the stock market, the most important organ is the stomach - it's not the brain." The only consolation I can offer at this stage is the fact that many of the fund managers that we use have delivered returns materially better than the broader markets (both share market and fixed interest market). It doesn't take the pain away, but it definitely helps a bit. Particular mention needs to be made of the Devon Trans Tasman Fund, Bentham Global Income Fund, Nikko AM Corporate Bond Fund, and Clarity Global Share Fund - these funds have stood out amongst peers. The other slight consolation is the fact that interest rates have risen so sharply and so quickly, that New Zealand fixed interest (bonds) look like good value to me again. I would expect sound returns from New Zealand bonds in the medium term (12 to 24 months) from here on in. Share markets are less predictable, so only time will tell how they play out from here. But based on the evidence of the past 12 bear markets, we are not too far off the average decline of 33%. Perhaps we don't go that far, perhaps we go past it - I'm not willing to try catch that falling knife. The approach now needs to be considered and deliberate - stick to your strategy, re-visit your risk profile, and re-balance your portfolio systematically. Here are the numbers for the past 30 days: |

||||||

|

||||||

In terms of your Select Wealth Management portfolio, you will be receiving your performance reports for the June quarter next month. Once again, this will not make for pleasant reading - be prepared. There has been a lot of consultation with our researchers JMI Wealth, and we are gradually making changes to portfolios as opportunities arise. In particular, we are moving away from global fixed interest in favour of New Zealand fixed interest. We also have some fund managers "on watch" and are slowly moving towards a more currency hedged position (given the relative strength of the US$). Finally, a quick update on our HUHA (Helping You Help Animals) Giving Back program. I am delighted to say that we have exceeded our expectations and managed to raise in excess of $2,500 for this great organisation. We have a couple of weeks to run on this campaign, and then we will be launching a new one for the second half of the year - I'll tell you all about it next month. To keep track of the Giving Back program visit https://mifinancialplanning.co.nz/giving-back.html As always, thank you for your continued support by introducing friends, family and colleagues to our business as prospective clients - I really appreciate it. Warm regards Dave and the team at Makowem & Isaacs Financial Planning dave@mifinancialplanning.co.nz |

||||||

|

||||||

This newsletter is intended for general distribution and does not constitute personal financial advice.