| Welcome to the July issue of the Select Wealth Management Dashboard Newsletter.

What a crazy few weeks it has been with an assassination attempt on Donald Trump. I find it difficult to believe that people get that exercised over politics that they would go to these extremes. Hopefully this event creates a pause for reflection for American voters, and they are able to gain perspective and become a bit more tempered in their behaviour. I would like to think that this could be a positive turning point, and that Americans will be a bit more unified. Time will tell if that is the case, or if this is just more fuel to the fire...

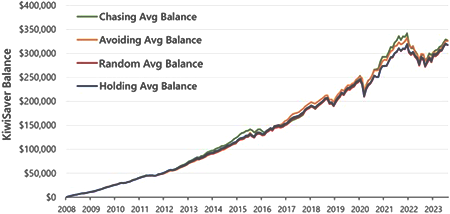

Locally, the Reserve Bank left the OCR (Official Cash Rate) unchanged at 5.5% at the meeting held on 10 July. They sighted that inflation was coming down, and expected it to continue coming down, forecasting the next reading to be 3.6% (as at 30 June). The actual reading came out on 17 July, and was 3.3% - lower than forecast. This implies that a rate cut may be coming sooner than previously thought - welcome news for those with a mortgage. My pick would be at least 1 rate cut before the end of this year, possibly 2. For this month's newsletter, I wanted to share a really good article I recently read written by Ben Brinkerhoff titled "What REALLY adds value when you choose a KiwiSaver scheme". Whilst this article was specific to KiwiSaver, the general principle applies to all forms of investment. I'll give you an abbreviated version with the main points, but you can read the full article here if you want. What Ben wanted to establish is whether or not there was a proven strategy for switching between KiwiSaver (or any other investment) providers. In particular, can you add value by changing providers based on past returns? For the purpose of his experiment, Ben used the "Aggressive Fund" category - a reasonable selection because aggressive funds typically have the highest returns and highest volatility. So this will create the biggest opportunity set if there was any benefit to be gained from any particular strategy. To be clear, this is not assessing if there is value from switching between asset allocations regularly (for example from Conservative to Growth one year, and then Growth to Balanced the next, etc.). This is simply assessing if there is value in changing from Provider A's Aggressive Fund to Provider B's Aggressive Fund regularly. Ben broke down investor behaviour into 4 categories as follows: Holding: An investor chooses a random fund at the start and never changes. Chasing: An investor looks at the last 12 months of cumulative returns and switches to one of the top 10% of best performing funds every 12 months as if trying to "chase" good returns. Avoiding: An investor looks at the last 12 months of cumulative returns and switches to one of the bottom 10% of worst performing funds every 12 months as if trying to find funds more likely to "bounce back". Random: An investor randomly selects a new fund every 12 months. The assumption is that the investor contributes $1,000 per month from January 2008 to August 2023. The trial is run 100 times, and the average results used. Intuitively, you would think that the Chasing strategy would result in the best outcomes, right? We are all susceptible to this strategy - it's difficult to do nothing when you see superior recent returns from other providers. The temptation is always to switch to the fund that did best last year. Or perhaps if you are a contrarian, you believe the Avoiding strategy would yield the best results - try to catch the funds with the big bounce back. Well, here are the actual results:

As you can see, there are no clear winners. Ironically, all 4 strategies result in an almost identical outcome over that time period. In fact, from 2008 to 2023, you get an almost identical $326,112 balance from Avoiding as the $326,767 you get from Chasing. And Random and Holding are only marginally behind that. So clearly, switching provider is not as beneficial as perhaps you might think. So what does matter then? Well, in my opinion, the more important issues are:

In terms of the markets, the past 30 days have been good for most share markets. The New Zealand market led the way with a gain of 5.41%, much of this driven by the prospect of falling interest rates in the near term. At the same time, the NZ$ weakened against all trading partners (again the prospect of lower interest rates in New Zealand pushing foreign money back off-shore). This combination of strong markets and a week currency has resulted in strong portfolio returns - particularly since 1 July. Long may it continue. Mortgage and term deposit rates also edged down, and house prices remain steady. Here are the numbers for the past 30 days: |

||||||

|

||||||

In terms of your Select Wealth Management portfolio, you will shortly receive your performance report for the June quarter (if you haven't already). The June quarter was soft, but the 1 year number to 30 June is still very healthy. We remain very comfortable with portfolios - particularly our fixed interest portfolios that will benefit in the short term from falling interest rates. Finally, a quick update on our Giving Back program. I am pleased to announce that for the second half of 2024, we will be supporting Life Flight. Life Flight are the organisation behind the Westpac Helicopter - a 24/7 emergency medical service that is entirely free of charge to the public. Amongst other things, this incredible service:

To learn more, you can visit https://www.lifeflight.org.nz This campaign is in memory of a friend of Makowem & Isaacs Financial Planning who sadly passed away recently, but had incredible service from Life Flight. As always, thank you so much for the introduction to your family and friends to allow us to continue this initiative - we really appreciate it. We will have a new campaign to share with you next month. In the meantime, to keep track of the Giving Back program visit https://mifinancialplanning.co.nz/giving-back.html That's all for now. Chat again soon Warm regards Dave and the team at Makowem & Isaacs Financial Planning dave@mifinancialplanning.co.nz |

||||||

|

||||||

This newsletter is intended for general distribution and does not constitute personal financial advice.