| Welcome to the February issue of the Select Wealth Management Dashboard Newsletter. As I write, Adrian Orr, Governor of New Zealand's Reserve Bank, has just announced a cut in the Official Cash Rate (OCR) from 4.25% to 3.75%. A quick refresher on what the OCR is and how it affects us:

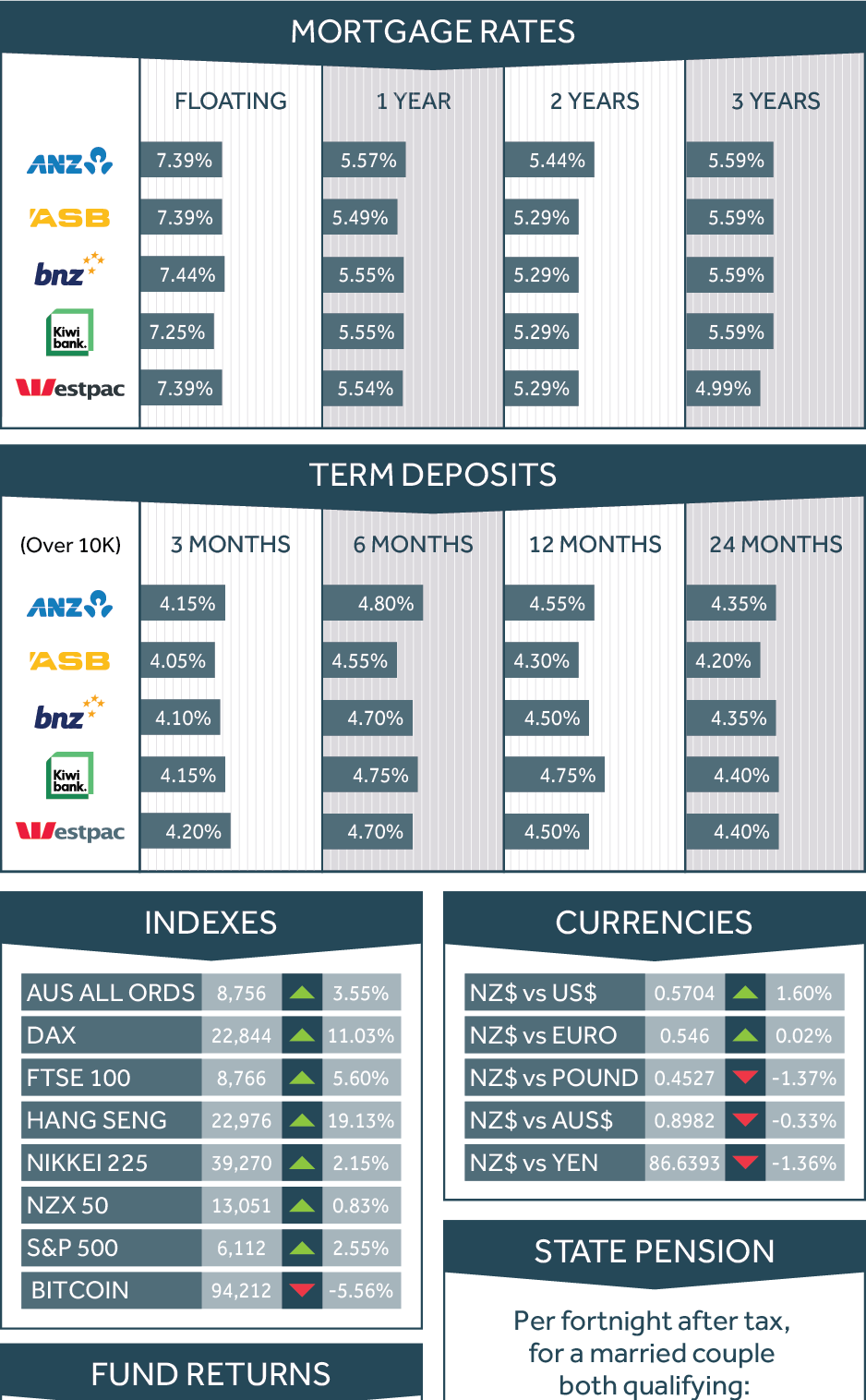

The OCR is the interest rate set by New Zealand's Reserve Bank. It influences the cost of borrowing and the return on savings. When the OCR is high, borrowing money via home loans or business loans becomes more expensive. This typically slows down spending, and as a result pushes inflation down. Conversely, a low OCR makes borrowing cheaper (think back to 1.99% mortgage rates in 2021). This encourages spending and investment, and as a result potentially increases inflation. The OCR also affects savings accounts, with higher rates offering better returns for savers and lower rates reducing incentives to save. Ultimately, the OCR plays a key role in shaping economic activity, employment levels, and the cost of living (inflation). Mr Orr's job is to get the balance right between cooling the economy when it's too hot, and stimulating it when it's too cold. His critics have argued for some time that he was too aggressive cutting rates post Covid, and then too aggressive raising rates when the economy was running hot and inflation was too high a few years later. Irrespective of your view on Mr Orr's performance, seeing the rate moving lower again is a very welcome relief for businesses and households. (Unfortunately, savers with term deposits pay the price here as their returns fall). With inflation currently at 2.2% per annum, comfortably in the 1% to 3% target range that the Reserve Bank has set, more rate cuts are expected in the year ahead with the forecast "terminal rate" being 3.10%. These OCR rate moves will filter through to the real economy over the next few months as banks lower mortgage rates, and households / businesses with fixed rate mortgages roll over onto lower rates and have some discretionary income to spend or invest elsewhere as a result. It's early days, but I suspect that the worst of the current downturn is now in the rearview mirror, and brighter times are on the horizon. This will be particularly good news for the hospitality, construction and retail industries who have been doing it really tough for a long time now, and who are often the first in line to benefit from discretionary income... The obvious question then is "how should you react from an investment perspective?". Surely a development like this seems to warrant some action. My answer is the same as always. Unless there has been significant changes in your personal situation, there's no need to change your long-term plan. Your investment objectives and risk tolerance should not have been influenced by this move in the OCR - these things are entirely unrelated. If you have a robust financial plan which includes a retirement cashflow projection and a well-diversified investment portfolio, you have already laid the foundation for a secure financial future - irrespective of what the OCR does on any given day. The same principle applies to a whole raft of other risks - political changes (red or blue), geopolitical developments (ceasefire deals in Gaza and Ukraine), trade developments (tariffs), the list goes on. I don't know with any degree of confidence how these things will affect investment markets. And I reckon anyone who gives you a confident answer is still just guessing. No one truly knows, and it's impossible to predict what might emerge next and how it will impact different parts of the market. So, the best thing to focus on is the things you have control over - your retirement goals, and your risk tolerance. And in considering these, it's worth keeping in mind that usually "the past is not as good as you remember, the present is not as difficult as you think, and the future won't be as bad as you worry." In terms of the markets, the past month has been very strong for share markets. All markets are up with Hong Kong's Hang Seng delivering a staggering 19% return, and Germany's Dax 11%. New Zealand's NZX50 was the worst performing with a very respectable 1% for the month. Mortgage and term deposit rates continue to decline. In fact by the time you receive this, they may be even lower in response to the OCR reduction. Interestingly, foreign exchange rates with major trading partners were reasonably muted after the OCR announcement. (Often big moves in the OCR rate can influence exchange rates as institutions move money from currencies with lower interest rates to those with higher interest rates). House prices drifted a bit lower, and Bitcoin fell by 5%. Here are the numbers: |

||||||

|

||||||

In terms of your Select Wealth Management portfolio, there have been no material changes over the past month. Performance remains in line with our expectations, and our panel of fund managers remain appropriate. Scottish Mortgage Trust has been the best performer in recent times up 22% in the past quarter and 46% over the past 12 months. In the Australasian shares sector, the Milford Dynamic Fund has been best with 5% for the quarter and 15% for the year. Finally, a quick update on the Giving Back campaign. We've had a good start to the campaign for Lower Hutt Woman's Refuge and are up to $450 already. As always, thank you for the referral of family and friends which enables us to continue this initiative. To keep track of the Giving Back program visit https://mifinancialplanning.co.nz/giving-back.html to learn more in the meantime. That's all for now. Chat again soon Warm regards Dave and the team at Makowem & Isaacs Financial Planning dave@mifinancialplanning.co.nz |

||||||

|

||||||

This newsletter is intended for general distribution and does not constitute personal financial advice.