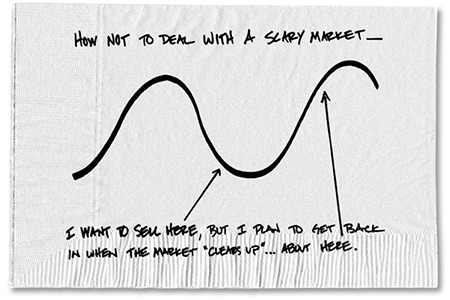

These are extraordinary times indeed. Further to the message I sent to you earlier in the week, I can not emphasize enough how important it is to avoid the trap of making a re-active decision now. Carl Richards sums it up best with this illustration:

Last month I wrote that I was optimistic that the Coronavirus would not be a “material issue” moving forward. I was wrong. This has now been declared a pandemic, and every day we hear about the impact it is having in various different countries – events being cancelled, businesses being suspended, cities being brought to a stand-still. Spare a thought for those who have had their lives disrupted – they will be hoping the scientists are working overtime to find the solution to the problem (which no doubt is just a matter of time). The virus (along with a combination of other factors) has resulted in some extremely violent moves in shares markets (both up and down). To illustrate the point, let’s look at the movements of the S&P500 (the best measure of the American share market). Since the volatility began on about the 20th of February, there have been trading days that have resulted in significant moves – both up and down:

If you had been trying to “time the market”, you are just as likely to miss a good day as you are to avoid a bad day. Worst case scenario, you could trade out the best day (+5.0%) for the worst day (-8.9%). The cost of this to you would be a total of 13.9% - a staggering cost as a result of a reactive decision that was out by 1 single day. It simply doesn’t work. A better way of thinking of this is to consider it in terms of time. How many years would you have to put your money in a 1 year term deposit before you recover your 13.9%. Well, assuming you could achieve 2% after tax from this deposit (which is unlikely moving forward), it would take a painfully long 8 years to recover this loss. Avoiding this loss puts you 8 years ahead. I accept that this is a challenging time as an investor, but the best course of action at this stage is to sit tight. Nobody knows what the market will do today, this week, or even in the next 6 to 12 months. However, what I do know is that your portfolio will behave exactly how it is built to behave. So if you were genuinely honest when we completed your risk profile questionnaire every year at the annual review, you can rest assured that your portfolio will remain within the parameters that you set in this risk profile. And as is the case with everything else, this too will come to pass. I continue to monitor your portfolio daily. Some buying opportunities are starting to present, and it may be that I recommend we “re-balance” your portfolio the in the next short while. If this is required, I will be in contact with you again with a clear recommendation specific to your portfolio. If you do not hear from me, then no action is required. Below are the numbers for the past 30 days. They are ugly – there is no other way to describe them. (When looking at these numbers, it is important to remember that not all of your investment is in share markets. Some is in cash, fixed interest and property, so your returns will not reflect the numbers you see below). Mortgage and deposit rates continue to come down, and it is reasonable to assume that the Reserve Bank will cut the Official Cash Rate again in the foreseeable future (as is happening in many other countries). |

||||||||||

|

||||||||||

Finally, a quick update on our Giving Back program. Unfortunately for Kapiti Birthright, the events of the past month have consumed all of our resources so the Giving Back Program has been on the back burner. We are behind on our target, but hope to get back on track within a couple of months once the dust starts to settle. Despite this fact, I still want to say thank you for the referrals of your friends, family and colleagues – keep ‘em coming. You can follow progress of the campaign at https://mifinancialplanning.co.nz/giving-back.html Warm regards Dave and the team at Isaacs Financial Planning dave@mifinancialplanning.co.nz |

||||||||||

|

||||||||||

This newsletter is intended for general distribution and does not constitute personal financial advice. Copy of my primary disclosure statement and secondary disclosure statement.