| Welcome to the August issue of the Dashboard Newsletter. For this month's newsletter, I'll start with the surprise interest rate cut from the Reserve Bank of New Zealand. On the 7th of August, the Reserve Bank of New Zealand reviewed the Official Cash Rate (OCR) as it does every 6 weeks. It was expected that the rate could potentially be cut, with most market commentators picking a 0.25% cut (the rest picking no change). However, governor Adrian Orr surprised the market by cutting the rate by 0.50% - something that has only happened once in the past 10 years. That takes the OCR to 1.00% - the lowest it has ever been in history.

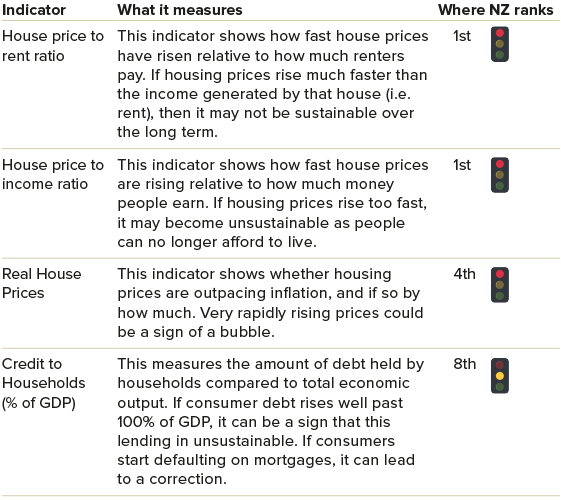

The effect this had was almost immediate. The NZ$ weakened significantly against most of its trading partners, falling by as much as 2% against the US$ immediately after the announcement. The New Zealand share market (NZX50) jumped 2% on the day. Some of the major New Zealand banks announced cuts in their mortgages rates, and also reduced their term deposits rates. So this rate cut was a significant event with significant impacts. There is a lot of talk now about the OCR falling even further – some market commentators picking as low as 0% or even negative. Personally I find this astounding, and I don't think it's going to happen. So what does this rate cut actually mean in the real world? Well, in the short term it was a nice little shot in the arm for markets. Companies (think Air New Zealand, the Warehouse, IceBreaker) can now borrow money at a lower cost than before, so it costs them less to service their debt. Less money spent on interest costs means more profits. So good for companies. Consumers with mortgages (you and I) have to pay less interest on our mortgage, so we have more money to spend on discretionary goods – a holiday flying Air New Zealand, a new BBQ for summer from the Warehouse, or a nice IceBreaker jacket. Good for us, and even better for the companies. But what about the people with no mortgage and money in term deposits (like many of our clients). They are now earning less interest on their term deposits. This encourages them to consider other investments options – possibly shares in Air New Zealand, The Warehouse and IceBreaker... This drives up share prices, and gives these companies more capital to grow their businesses. More good news for those companies, and their shareholders. This is the rational behind rate cuts – to stimulate the economy. And in the short term it works. So the question is how long does this effect continue. At some point, rates can't go any lower and this stimulus comes to an end. In fact at some point rates will have to go up, potentially resulting in the opposite effect of the above. So despite all the media rhetoric, I believe common sense will prevail and interest rates will stabilise in the medium term (in New Zealand and the rest of the world). Perhaps one more cut in the short term, and then back to a more prudent approach. I think the central banks around the world will want to ensure they keep some candy in the jar in case they need it at a later date. On a slightly different topic (but still very much related), Bloomberg recently released some data on housing markets around the world. The title of the paper was "The Countries with the Highest Housing Bubble Risks". They came up with 4 indicators to measure the value of housing markets in different countries, with the objective of identifying which markets looked over-valued and at risk. The indicators are:

In their survey, Bloomberg found only 2 countries that fell into the "danger zone" in all four of these categories – Canada and New Zealand. By their reckoning, New Zealand is the second most over-priced property market in the world (second only to Canada). Their conclusion is that "Canada and New Zealand may be overdue a correction in housing prices". This is consistent with the information coming out of QV, which shows that property values in Auckland have fallen by 4.7% (or $51,479 per property) over the past year. Given this backdrop, I find it hard to imagine that the Reserve Bank are going to cut rates too much further. Lower mortgage rates drive property values up – something that New Zealand can ill afford. It wasn't that long ago that every other newspaper headline was about house prices being too high and the housing affordability issue in New Zealand. This has finally started to correct itself, and the Reserve Bank would surely not want to interfere with this process by fuelling the market with lower mortgage rates. I once read that "he who lives by the crystal ball is destined to eat ground glass", so I typically avoid trying to "pick markets" at all costs. Time will tell how my thoughts on these interest rates play out – maybe I'm right, maybe I'm not. In the meantime, it doesn't change my investment approach. The best strategy still remains to have a disciplined approach, and to focus on your own personal objectives and tolerance towards risk. Making changes to a portfolio now based on crystal ball gazing (about interest rates, property values, or any other opinion) exposes you to the risk of your portfolio not meeting your expectations and you achieving your goals. This is not a risk worth taking. All said and done, markets were mixed over the past 30 days. Most share markets were down between 2% and 5% (New Zealand being the only exception up 1.4%). Hong Kong was the outlier down by as much as 11%. However, these negative returns from the share markets were off-set by the NZ$ weakening against most of its trading partners. The exception here was the GBP, presumably because of the looming Brexit D Day of 31 October. As I mentioned before, mortgage and deposit rates fell slightly over the past 30 days. Here are the numbers: |

||||||

|

||||||

In terms of your Select Wealth Management portfolio, I am pleased to confirm that returns have been in line with expectation, and the platform continues to meet our expectations and deliver a high quality service. We continue to look for ways to drive costs down and continually pressure fund managers available through Select Wealth Management to discount their fees. I am pleased to confirm that in the past month several more fund managers have confirmed fee rebates for Select Wealth Management clients. This is a fantastic outcome, and you will see these fee rebates coming through on your next quarterly report. Finally, a quick update on our Giving Back program for Hutt Valley Gymnastics. After a slow start to the campaign, I am pleased to report that the past month has seen us get back on track to reaching our target of $2,500. You can learn a bit more at www.mifinancialplanning.co.nz/giving-back.html. Once again, thank you so much for the referrals of your friends and family so that we can continue to fund this program - we really appreciate it. Warm regards Dave and the team at Isaacs Financial Planning dave@mifinancialplanning.co.nz |

||||||

|

||||||

This newsletter is intended for general distribution and does not constitute personal financial advice. Copy of my primary disclosure statement and secondary disclosure statement.